{kind=link}

Manufacturing and gross sales of all autos and “new vitality autos” (NEVs) in China, from Nationwide Bureau of Statistics and China Affiliation of Vehicle Producers information through Wind Monetary Terminal. NEVs embody battery electrical autos and plug-in hybrids. The best-hand facet reveals the share of NEVs out of all new autos bought, and the cumulative share over the previous 10 years, as an indicator of the share of NEVs out of autos on the highway. Chart by Carbon Transient.

China’s EV market is very aggressive, with not less than 94 manufacturers providing greater than 300 fashions. Home manufacturers account for 81 per cent of the EV market, with BYD, Wuling, Chery, Changan and GAC among the many prime gamers.

Sustaining this development has required main funding in manufacturing capability.

This evaluation estimates investments in EV manufacturing capability based mostly on a research by China Worldwide Affiliation for Promotion of Science and Expertise (CIAPST), which put funding in EV manufacturing at 0.7tn yuan in 2021.

The evaluation assumes that EVs accounted for the entire development in funding in automobile manufacturing capability reported by China’s nationwide bureau of statistics (NBS) in 2022 and 2023, whereas funding in typical autos was steady

This means that funding in EV manufacturing reached CNY 1.2tn yuan in 2023. That is prone to be conservative, as a result of manufacturing volumes for combustion engine autos are falling, implying a corresponding fall in funding.

This evaluation accounts for the growth of battery manufacturing capability individually – alongside electrical energy storage – despite the fact that it’s being pushed by the expansion in EV manufacturing.

The evaluation estimates the worth of EV manufacturing, together with each home gross sales and exports, based mostly on automobile manufacturing volumes from NBS and the reported common EV worth.

These EV costs embody the worth of batteries produced for EVs, so the worth of battery manufacturing just isn’t included individually.

In the meantime, EV charging infrastructure is increasing quickly, enabling the expansion of the EV market. In 2022, greater than 80 per cent of the downtown areas of “first-tier” cities – megacities reminiscent of Beijing, Shanghai and Guangzhou – had put in charging stations, whereas 65 per cent of the freeway service zones nationwide offered charging factors.

Greater than 3m new charging factors have been put into service throughout 2023, together with 0.93m public and a couple of.45m personal chargers. The accrued whole by November 2023 reached 8.6m charging factors.

This evaluation places funding in EV charging infrastructure at 0.1tn yuan in 2023, based mostly on an estimated common price of 30,000 yuan per charging level.

China’s vitality depth discount targets have put strain on industries to scale back their vitality use per unit of output, spurring funding in additional environment friendly processes.

For this evaluation, the scale of the marketplace for vitality service firms is used as a proxy for funding in vitality effectivity in industries and buildings. This market grew to an estimated 0.6tn yuan in 2023, up from 0.5tn yuan in 2022, based mostly on the income development of the highest 10 listed vitality service firms ranked by market capitalisation, for the primary two or three quarters of 2023.

Over the previous 20 years, China’s vitality service sector has skilled fast growth, rising from 1.8bn yuan in 2003 to 607bn yuan in 2021. Funding within the industrial service sector has been a key driver, accounting for about 60 per cent of the entire funding.

Nevertheless, 2022 noticed a big downturn within the industrial vitality service output, influenced by poor industrial development, despite the fact that the constructing service sector continued increasing.

This evaluation places China’s funding in constructing vitality effectivity at 80bn yuan per 12 months. The nation’s 14th five-year plan for vitality financial savings in buildings and improvement of “inexperienced buildings” targets 80m sq. metres per 12 months of renovated and newly constructed inexperienced buildings.

In contrast with the just about 1,000m sq. metres of constructing area accomplished yearly, this can be a small share, and accordingly, the estimated worth of whole investments is modest.

China is quickly scaling up electrical energy storage capability. This has the potential to considerably cut back China’s reliance on coal- and gas-fired energy vegetation to satisfy peaks in electrical energy demand and to facilitate the combination of bigger quantities of variable wind and solar energy into the grid.

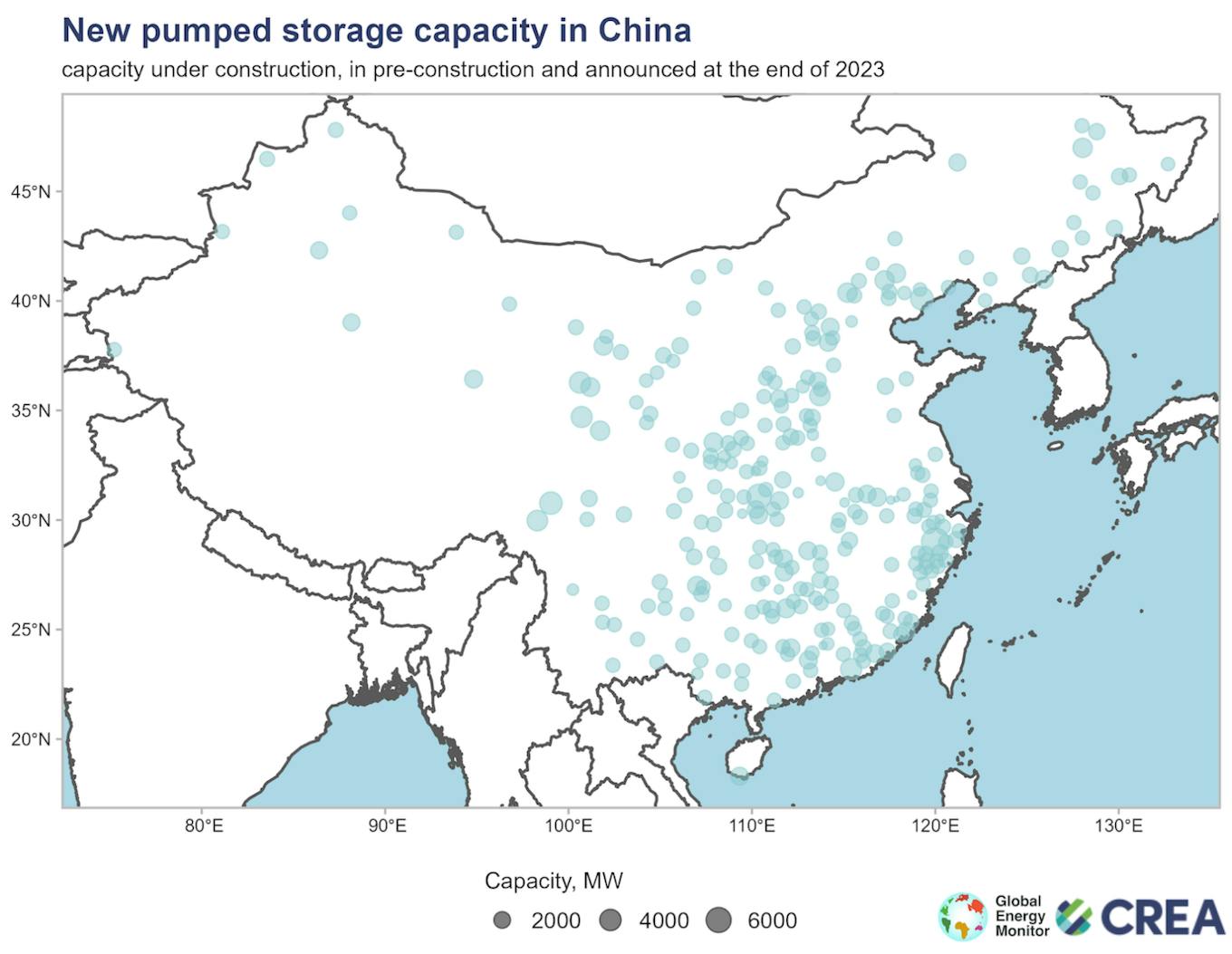

The development of pumped hydro storage capability elevated dramatically within the final 12 months, with capability beneath building reaching 167GW, up from 120GW a 12 months earlier.

This development is illustrated within the determine under, which reveals pumped hydro capability beneath building or in earlier phases of improvement on the finish of 2023.

Capability of pumped hydro storage initiatives beneath building or in earlier phases of improvement on the finish of 2023, GW. Supply: International Power Monitor international hydropower tracker.

Knowledge from International Power Monitor identifies one other 250GW in pre-construction phases, indicating that there’s potential for the present surge in capability to proceed.

For this evaluation, estimated annual investments in pumped storage are assumed to be proportional to the capability beneath building, whereas the reported building price of 6 yuan per watt is unfold over three years. This means that funding in 2023 amounted to 0.3tn yuan.

Development of latest battery manufacturing capability was one other main driver of investments, estimated at 0.3tn. That is based mostly on the added capability reported by the China Automotive Energy Battery Business Innovation Alliance and estimated common funding prices per unit of manufacturing capability, taken from a compilation of publicly reported undertaking prices.

Funding in electrolysers for “inexperienced” hydrogen manufacturing nearly doubled year-on-year in 2023, reaching roughly 90bn yuan, based mostly on estimates for the primary half of the 12 months from SWS Analysis. Analyst stories and compilations of initiatives printed in information media put far bigger numbers on China’s investments in inexperienced hydrogen, however these usually embody the spending on electrical energy technology, which on this evaluation is accounted for individually.

Funding in “new vitality storage applied sciences” – a classification dominated by batteries – greater than doubled in 2023, reaching 75bn yuan. This estimate relies on newly added capability in 2023 reported by China Power Storage Alliance and common funding prices calculated from Nationwide Power Administration information.

Railways

China’s ministry of transportation reported that funding in railway building elevated 7 per cent in January–November 2023, implying funding of 0.8tn for the complete 12 months. This consists of main investments in each passenger and freight transport. Funding in roads fell barely, whereas funding in railways general grew by 22 per cent.

The share of freight volumes transported by rail in China has elevated from 7.8 per cent in 2017 to 9.2 per cent in 2021, because of the fast improvement of the railway community.

In 2022, some 155,000km of rail traces have been in operation, of which 42,000km have been high-speed. That is up from 146,000km of which 38,000km have been high-speed in 2020.

The worth of passenger and freight transportation on China’s railways elevated by 39 per cent year-on-year in 2023, reaching almost 1tn yuan.

Nuclear energy

In 2023, 10 nuclear energy items have been authorised in China, exceeding the anticipated fee of 6-8 items per 12 months set by the China Nuclear Power Affiliation in 2020 for the second 12 months in a row.

There are 77 nuclear energy items which can be at the moment working or beneath building in China, the second-largest whole on this planet. The entire yearly funding in 2023 was estimated for this evaluation at 87bn yuan, a rise of 45 per cent year-on-year, based mostly on information for January–November from the Nationwide Power Administration.

The very best numbers of nuclear initiatives are situated in coastal provinces with giant concentrations of heavy trade, reminiscent of Guangdong, Fujian and Zhejiang, as the event of inland nuclear energy initiatives stays stalled.

These provinces get round 20 per cent of their electrical energy from nuclear energy and proceed to increase the expertise as a part of their efforts to chop emissions from their energy sectors.

Electrical energy grids

China’s power-sector improvement plans embody a significant enhance in inter-provincial electrical energy transmission capability and quite a few long-distance transmission traces from west to east.

State Grid, the government-owned operator that runs the vast majority of the nation’s electrical energy transmission community, has a goal to lift inter-provincial energy transmission capability to 300GW by 2025 and 370GW by 2030, from 230GW in 2021. These plans play a significant position in enabling the event of unpolluted vitality bases in western China.

China Electrical energy Council reported investments in electrical energy transmission at 0.5tn yuan in 2023, up 8 per cent on 12 months – simply forward of the extent focused by State Grid.

Why clear vitality took off in 2023

The clean-energy funding increase in 2023 is the result of a significant pivot in China’s macroeconomic technique. As this evaluation reveals, funding flowed from actual property into manufacturing – primarily within the clean-energy sector.

Whole funding within the manufacturing trade elevated by 9 per cent year-on-year in 2023, whereas funding within the energy and warmth sectors climbed 23 per cent. These will increase have been completely as a consequence of development in funding in clear vitality, with funding in different areas falling. Subsequently, China’s pivot into manufacturing was, in actuality, a pivot to cleantech manufacturing.

The explanation for this pivot was the contraction within the real-estate sector, the place funding fell by 10 per cent year-on-year in 2022 and one other 9 per cent in 2023. Whereas this drop was consistent with the authorities’s intention to handle monetary dangers and extra leverage within the sector, it left a main gap in mixture funding demand and within the income of China’s native governments.

Native governments have been beneath strain to draw funding, which means that they supplied beneficiant subsidies and helped prepare financing.

The central authorities, for its half, eased private-sector entry to monetary markets and financial institution loans in the course of the Covid-19 pandemic, facilitating the expansion of the clean-energy sector.

In contrast to the state-owned corporations dominating conventional industries, the low-carbon sector, largely composed of personal firms, gained entry to beforehand constrained credit score.

The importance of this financial shift is mirrored not solely within the figures revealed by this evaluation but in addition within the language being utilized by Chinese language media.

The three largest of clean-energy sectors by worth, particularly photo voltaic, storage and EVs, are being known as the “new three”, in distinction to the “outdated three” – clothes, residence home equipment and furnishings.

This pivot was solely potential as a result of China’s clean-energy insurance policies and wider industrial coverage had constructed the muse and scaled up these sectors in order that they have been primed for fast development.

The post-Covid credit score “push” for clear vitality development additionally coincided with a requirement “pull”, pushed by falling prices and the elevated competitiveness of low-carbon applied sciences in opposition to fossil fuels as a consequence of technological developments.

Furthermore, the announcement in 2020 of the 2060 carbon neutrality goal had raised expectations and offered the political sign for the scale-up.

What clean-energy development means for China – and the world

Clear expertise has been an vital a part of China’s vitality coverage, industrial technique and local weather change efforts for a very long time. Final 12 months marked the primary time that the sector additionally grew to become a key financial driver for the nation. This has vital implications.

China’s reliance on the clean-technology sectors to drive development and obtain key financial targets boosts their financial and political significance. It might additionally assist an accelerated vitality transition.

The huge funding in clear expertise manufacturing capability and exports final 12 months implies that China has a significant stake within the success of unpolluted vitality in the remainder of the world and in build up export markets.

For instance, China’s lead local weather negotiator Su Wei just lately highlighted that the aim of tripling renewable vitality capability globally, agreed within the COP28 UN local weather summit in December, is a significant profit to China’s new vitality trade. It will possible additionally imply that China’s efforts to finance and develop clear vitality initiatives abroad will intensify.

Globally, China’s unprecedented clean-energy manufacturing increase has pushed down costs, with the price of photo voltaic panels falling 42 per cent year-on-year – a dramatic drop even in comparison with the historic common of round 17 per cent per 12 months, whereas battery costs fell by an excellent steeper 50 per cent.

This, in flip, has inspired a lot quicker take-up of clean-energy applied sciences.

Projections of solar energy deployment, specifically, have been upended. The IEA’s newest World Power Outlook launched an extra international vitality situation simply to have a look at the implications, projecting that if international deployment of solar energy and grid-connected batteries follows the growth of producing capability, then international power-sector coal use and carbon dioxide emissions may very well be a large 15 per cent decrease than within the base case by 2030. A lot of the further deployment of photo voltaic within the IEA’s revised projections is in China.

Even with the elevated deployment, nonetheless, there’s a restrict to how a lot solar energy, batteries and different clear expertise will be absorbed, because the manufacturing growth has already saturated many of the international market.

Because of this the growth will run into overcapacity, if maintained. Alternatively, with a purpose to hold driving development in funding, clean-technology manufacturing would want to not solely take up as a lot capital because it did in 2023, however hold rising funding 12 months after 12 months.

The clean-technology funding increase has offered a brand new lease of life to China’s investment-led financial mannequin. There are new clean-energy applied sciences the place there’s scope for growth, reminiscent of electrolysers.

Ultimately, nonetheless, completely new sectors should be discovered for funding – or China’s financial mannequin should be remodeled as soon as there’s nowhere left for funding to stream.

The manufacturing increase additionally cements China’s dominant place in clean-energy provide chains. Different international locations due to this fact face a selection of whether or not they need to profit from the low-cost provide of photo voltaic panels, batteries, EVs and different clean-energy expertise from China.

The choice is diversifying their provide and paying the price of constructing new provide chains, within the type of subsidies and import tariffs required to allow home producers or producers in third international locations to compete in opposition to Chinese language suppliers. Such efforts would additional enhance provide and push down international costs even additional.

This story was printed with permission from Carbon Transient.