{kind=link}

Join each day information updates from CleanTechnica on e-mail. Or observe us on Google Information!

A brand new report explores how Europe can efficiently construct a sustainable battery worth chain

Govt abstract

As Europe is decarbonising its financial system, it’s dealing with a monumental problem to rebuild the fossil-based system right into a carbon free one. Batteries and the supplies that go into making them are central to our effort to wash up automobiles, vehicles and buses in addition to to increase renewable vitality networks. A yr in the past, as T&E estimated that two-thirds of Europe’s introduced battery plans are in danger, the EU introduced a raft of measures in response to the US Inflation Discount Act. So one yr on, what does the progress in constructing battery provide chains appear like? This report analyses the progress, in addition to challenges related to onshoring this provide chain, offering an industrial footprint for governments to construct a neighborhood, resilient and sustainable battery provide chain.

Key findings embrace:

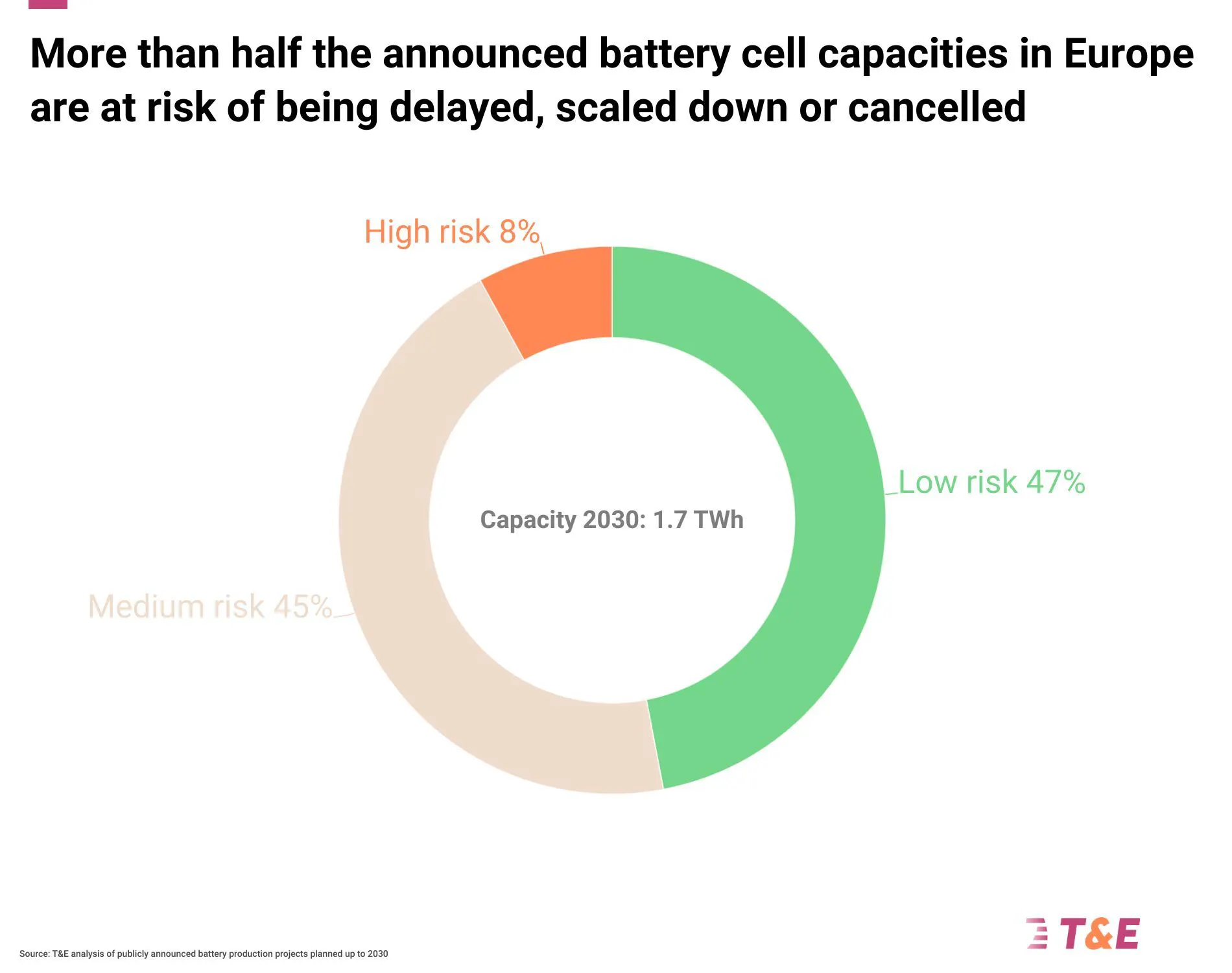

- Europe can turn out to be self-sufficient in battery cells by 2026, and manufacture most of its demand for key parts (cathodes) and supplies reminiscent of lithium by 2030. However over half of gigafactory plans in Europe stay prone to both being delayed or cancelled, down from near two-thirds a yr in the past.

- Onshoring the battery provide chain gives important local weather advantages: 37% discount in carbon emission when utilizing the EU grid, or 133 Mt of CO2 by 2030 in comparison with China. When counting on predominantly renewable vitality sources, the reductions double to 62%.

- Nonetheless, lots of the introduced initiatives stay unsure and, given the nascent nature of this business in Europe, wouldn’t occur with out stronger authorities motion.

- The commercial coverage blueprint ought to embrace sustaining the funding certainty (through the 2035 clear automobile aim), offering EU-level funding assist and stronger made in EU provisions for best-in-class initiatives.

Europe isn’t ranging from scratch. Years of bold coverage to safe a neighborhood electrical automobile market, in addition to the efforts of the European Battery Alliance, have resulted in dozens of battery investments and bulletins all through the provision chain.

Chapter 1

Vital native potential exists

Europe isn’t ranging from scratch. Years of bold coverage to safe a neighborhood electrical automobile market, in addition to the efforts of the European Battery Alliance, have resulted in dozens of battery investments and bulletins all through the provision chain.

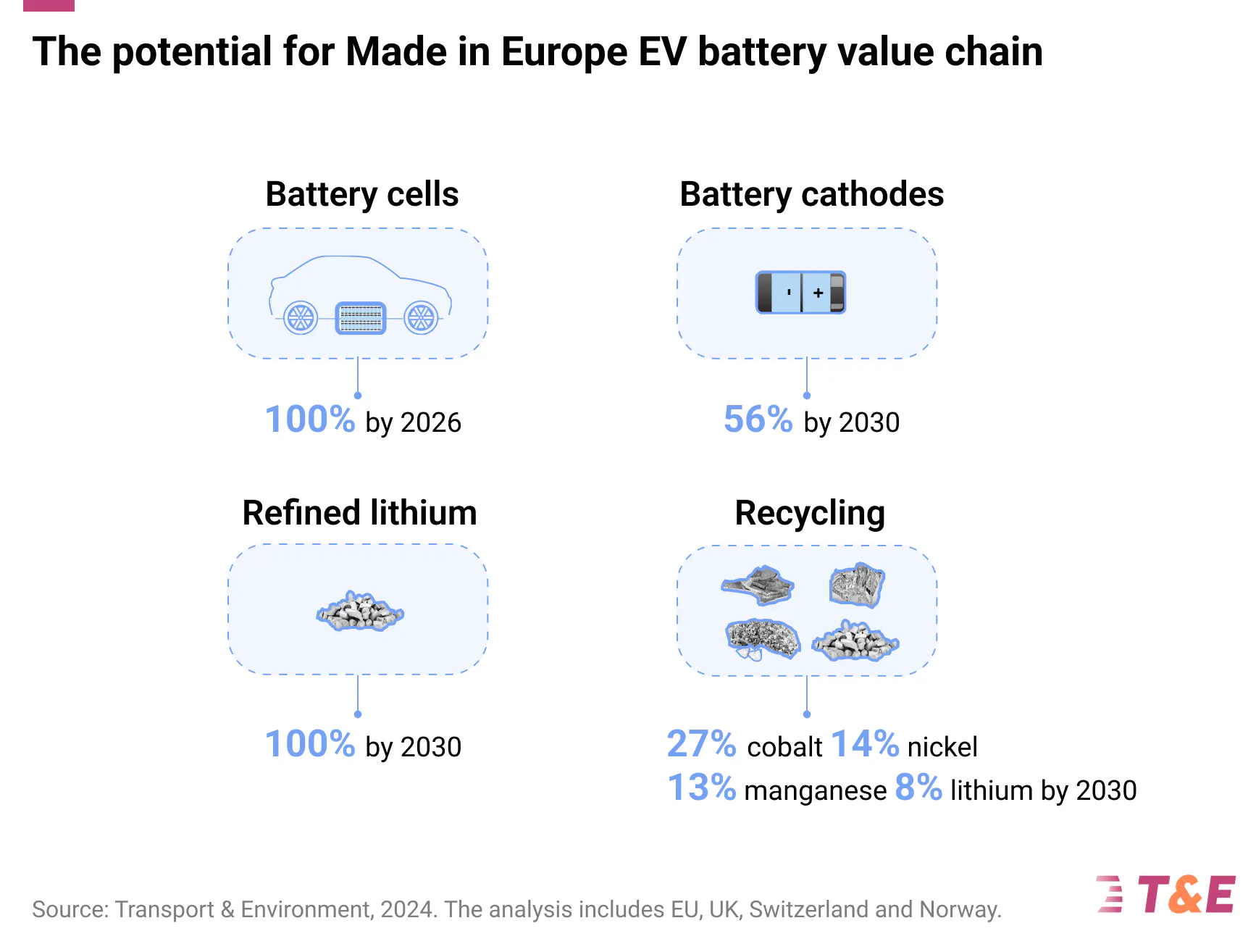

Based mostly on the most recent bulletins, Europe can:

- Grow to be self-sufficient in native battery cell provide from as early as 2026

- Provide over half (56%) of battery’s most useful parts – cathodes – by 2030, into which crucial minerals reminiscent of nickel and lithium are processed

- Provide all of its processed lithium wants by 2030, and

- Safe between 8% and 27% of battery minerals provide from domestically recycled sources by 2030.

However these plans are all at totally different levels of maturity and require long-term political imaginative and prescient and focused industrial technique to materialise. On high, Europe isn’t working in a vacuum: a fierce “battery arms race” is occurring the world over, from China’s overcapacity leading to imports of low-cost EVs and batteries into Europe to rising useful resource nationalism throughout the World South. The dangers to Europe’s onshoring ambition are many-fold.

A yr since T&E began assessing the viability of battery plans, over half of gigafactory plans in Europe stay prone to both being delayed or cancelled, down from near two-thirds a yr in the past. That is an enchancment of 15%. ACC in France kicked off manufacturing within the final yr, whereas Northvolt’s second gigafactory in Germany was saved because of the German state’s beneficiant subsidy to counter the US IRA. Due to an analogous assist bundle in France, Verkor is about to start out business manufacturing in France. However, some firms – notably Freyr and VW’s PowerCo – have downgraded their plans. Total, the capacities at low danger quantity to round 815 GWh, ample to energy 13.6 million electrical automobiles.

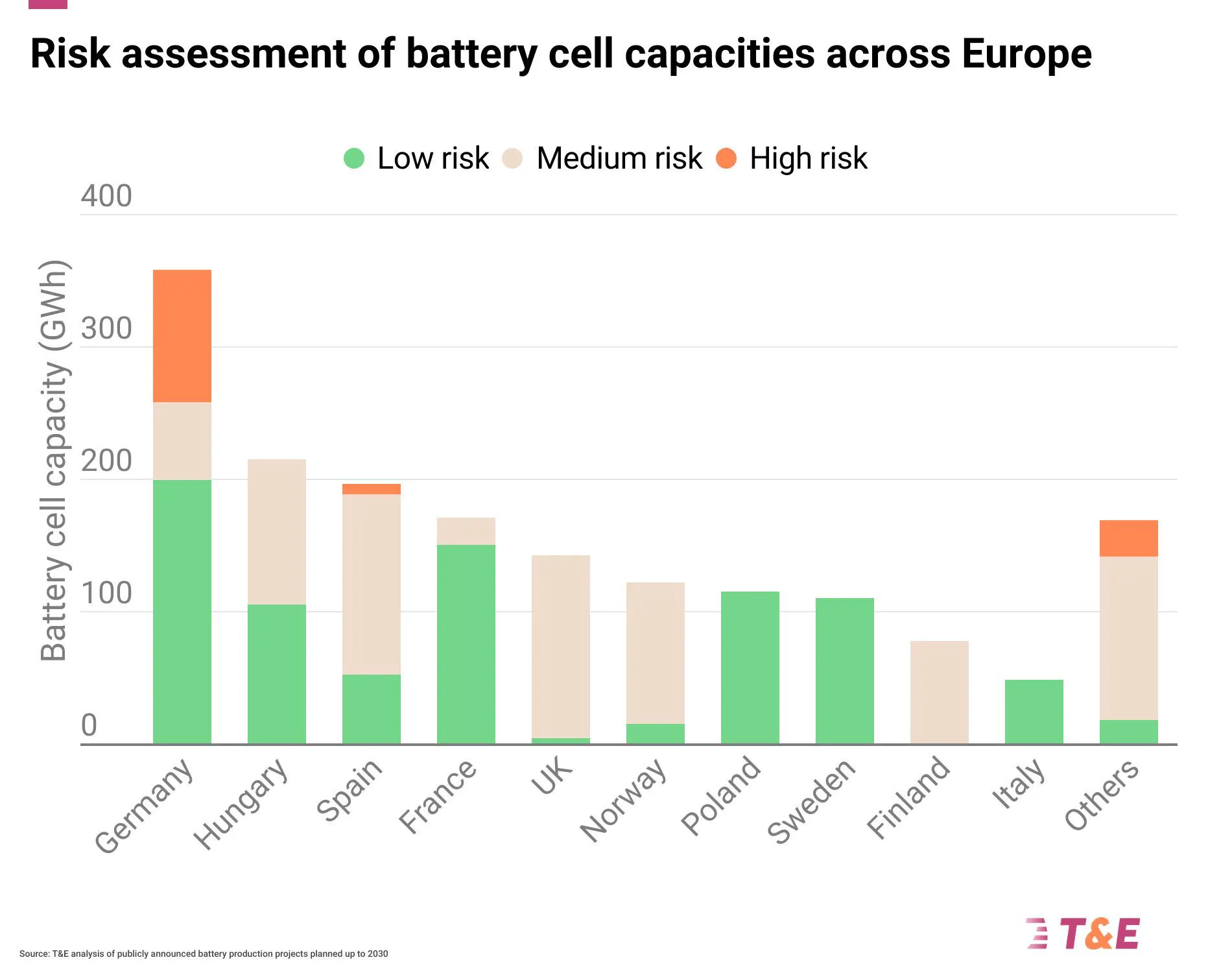

Throughout Europe, Finland, the UK, Norway and Spain, with initiatives by the Finnish Minerals Group, West Midlands Gigafactory, Freyr and Inobat, have the best shares of capability at excessive or medium danger. However, France, Germany and Hungary have made probably the most progress in securing capability in comparison with final yr.

Going additional mid- and up-stream reveals extra dangers. Whereas plans to construct cathode energetic materials amenities throughout Europe exist, these have skilled much less growth than cells, with the area dealing with crucial gaps when it comes to mission growth. These signify over half of the battery’s worth with their manufacturing nearly completely concentrated in China as we speak. This highlights the urgency of building home capabilities to permit Europe to seize the total worth chain. However solely Umicore in Poland and BASF in Germany have began business operations to date, with Northvolt piloting a small batch manufacturing in Sweden. Nonetheless, within the final 12 months numerous firms, predominantly Chinese language, have introduced plans to arrange cathode amenities on the continent.

Taking a look at battery metals, lithium refining initiatives maintain excessive potential for Europe’s self-sufficiency. From a really restricted lithium chemical substances manufacturing as we speak, the introduced capacities might cowl the area’s wants by 2030. The most important capacities are situated within the UK (e.g. Tees Valley Lithium and Inexperienced Lithium), Germany (e.g. Vulcan Vitality Assets and Livista Vitality) and France (e.g. Lithium de France and Imerys). However many of those initiatives are nonetheless in early levels of growth. Within the nickel area, the present nickel sulphate plans can probably cowl a fifth of future demand from electrical automobile and vitality storage batteries.

Chapter 2

The advantages of onshoring are important

Onshoring the battery provide chain gives extra management over how issues are executed. Native manufacturing means Europe can set and implement environmental and social requirements, in addition to stipulate the efficient and significant engagement of native communities. Localising the battery worth chain may also result in shorter provide chains and lowered transportation-related emissions, on high of Europe’s comparatively excessive share of renewables to learn cleaner processes.

From a pure local weather perspective, manufacturing a number of the extra vitality intensive and invaluable parts in Europe may even scale back carbon emissions. Producing battery cells domestically in comparison with China on common saves 20-40% of carbon emissions, whereas onshoring cathode manufacturing would save as much as a fifth moreover. Native sources of nickel could be 85-95% decrease in emissions than the present provide from Indonesia, whereas lithium will include an as much as 50% enchancment to Australian ore processed in China. Total, the carbon advantages of onshoring into Europe are within the order of 37% carbon emission discount based mostly on the EU grid, rising to over 60% when predominantly renewable vitality sources are used. In comparison with a totally imported provide chain, producing Europe’s demand for battery cells and parts domestically would save an estimated 133 Mt of CO2 by 2030, akin to the emissions produced by whole Chile or the Czech Republic in 2022.

Chapter 3

However it gained’t be simple

However reaping these local weather and industrial advantages is not going to be simple. Vital challenges in scaling the European battery worth chain exist. First, securing the battery uncooked supplies themselves. T&E estimates that the out there home provide from main mined and secondary sources can on common cowl 35%-70% of finish use battery demand (or 45%-100% of cathode processing demand) by 2030, however many mining initiatives stay unsure and face native opposition. In the end, a worldwide uncooked supplies technique and sharp diplomacy will likely be wanted to safe the supplies for Europe’s ambition with each Europe’s pursuits and native growth targets in thoughts.

One of many key questions requested is that if Europe can develop the experience and abilities obligatory to construct up this capability. Whereas some progress has been made on cell making (with over half of Europe’s wants already produced domestically by European and Asian firms), the midstream worth chain is much less sure. Nonetheless, T&E evaluation reveals that quite a lot of innovation and abilities can be found domestically. E.g. a lot progress is occurring within the space of lithium processing, with Europe being one of many main continents in creating the clear direct lithium extraction applied sciences (15% of all lithium initiatives plan to make use of that), and the primary continent that goals to commercialise the cleaner bioheap leaching route for nickel refining (in Finland).

Whereas China undoubtedly has a lead in cathode making, European firms do have the required experience in chemical substances and hydrometallurgy essential to scale this sector. The present efforts are concentrating on effectivity and course of step discount, in addition to utilizing cleaner processes, to cement a European edge. On abilities, T&E finds that whereas there’s a scarcity of direct metallurgical employees, the adjoining abilities will be drawn from the petrochemicals, prescription drugs and materials science sector amongst others. A few of these adjoining industries – notably oil and automotive catalysts – are anticipated to say no within the coming years, so provide a fantastic reskilling alternative.

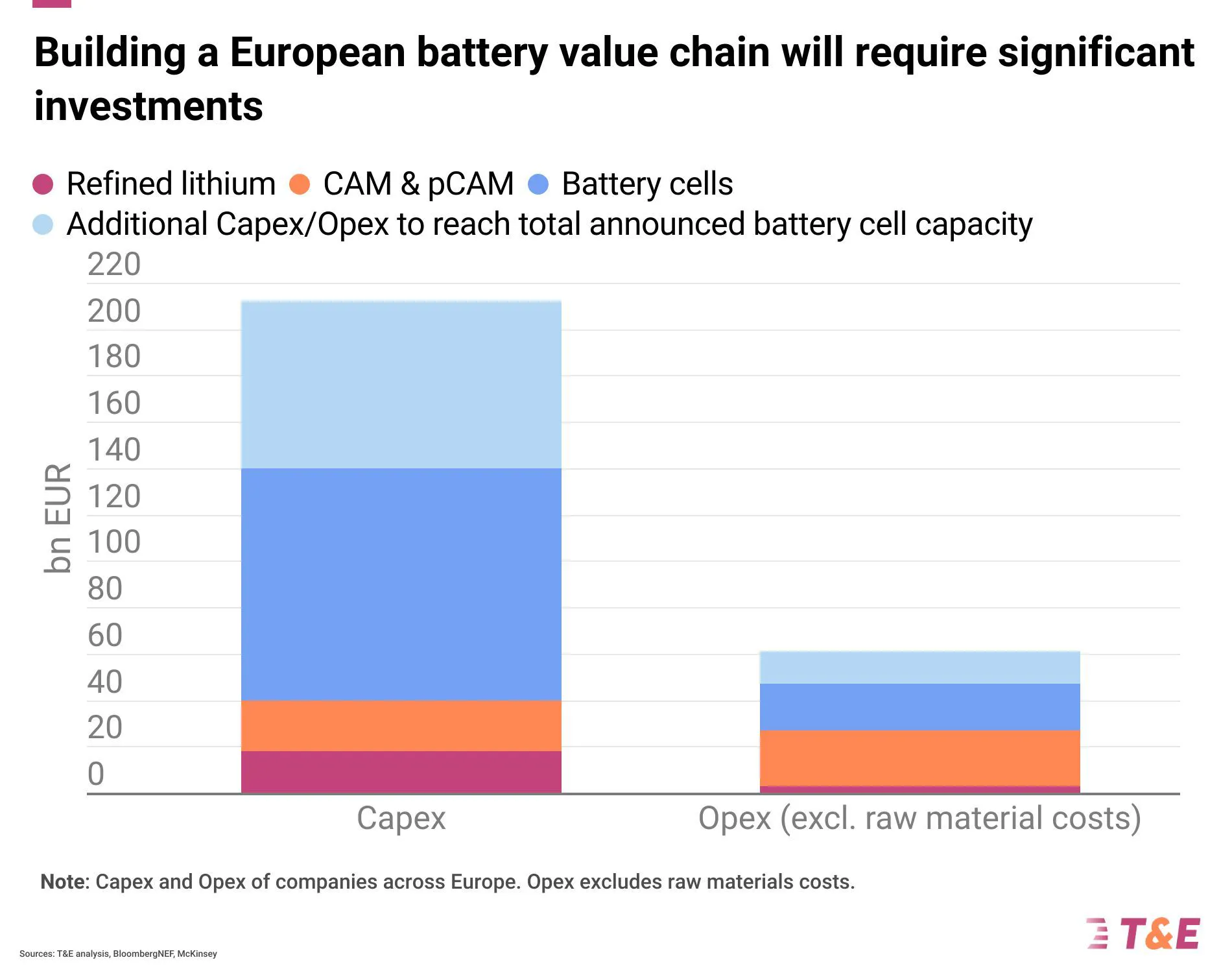

On the identical time, each capital expenditure (CAPEX) and operating, or operational (OPEX) prices, of constructing and operating battery cell, part and materials amenities are a number of the highest in Europe. This is because of much less experience constructing these amenities, in addition to because of larger vitality and labour prices (a minimum of in comparison with China). T&E estimates that creating all of the introduced plans for battery cell manufacturing, cathode and precursor amenities and lithium refining in Europe (together with non-EU nations) would require EUR 215 billion in CAPEX and EUR 61 billion in annual OPEX, coming primarily from personal funding. If Europe aimed, for instance, to match the operational assist offered below the US IRA, it could want to offer round EUR 2.6 bn in OPEX assist on an annual foundation alone.

Chapter 4

Key suggestions

In a nutshell, whereas the numerous potential to construct a neighborhood and clear battery provide chain exists, the dangers are manifold. With out political management and powerful insurance policies Europe will wrestle to create the enterprise case amidst the fierce world competitors.

T&E presents its personal industrial blueprint for the governments throughout Europe.

s Europe.

- Clear coverage and long-term imaginative and prescient are paramount to safe funding into battery provide chains. This contains the 2025-2035 automobile CO2 ambition that should stay unchanged, in addition to extra ambition to impress fleets and create a European compact BEV business.

- Strong insurance policies to safe native manufacturing, away from overreliance on imports. This contains sturdy sustainability necessities to reward native clear manufacturing (such because the upcoming battery carbon footprint guidelines), sooner implementation of initiatives below CRMA and NZIA and a revamped commerce coverage. Crucially, complete funding assist will likely be crucial to construct the provision chain throughout Europe, together with higher devices below the European Funding Financial institution and a shortly operationalised EU Battery Fund.

- All of this have to be executed sustainably, breaking with the previous practices in metallic provide chains the world over. This implies constructing the worldwide uncooked materials partnerships on excessive requirements and supporting native worth add in resource-rich nations. Europe also needs to decide to convey its personal mining practices according to world finest apply, notably on tailings administration.

Batteries, and metals that go into them, are the brand new oil. European leaders will want laser sharp focus, sturdy and joint up considering and, above all, stepping out of the consolation zone to succeed. The prices of failing are excessive and may end up in Europe dropping out on whole industrial sectors. Some progress has been made within the final yr, however the subsequent European Fee and Parliament have a monumental process of ending the job.

Report courtesy of Transport & Atmosphere

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

Newest CleanTechnica.TV Video

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.