Join day by day information updates from CleanTechnica on e mail. Or comply with us on Google Information!

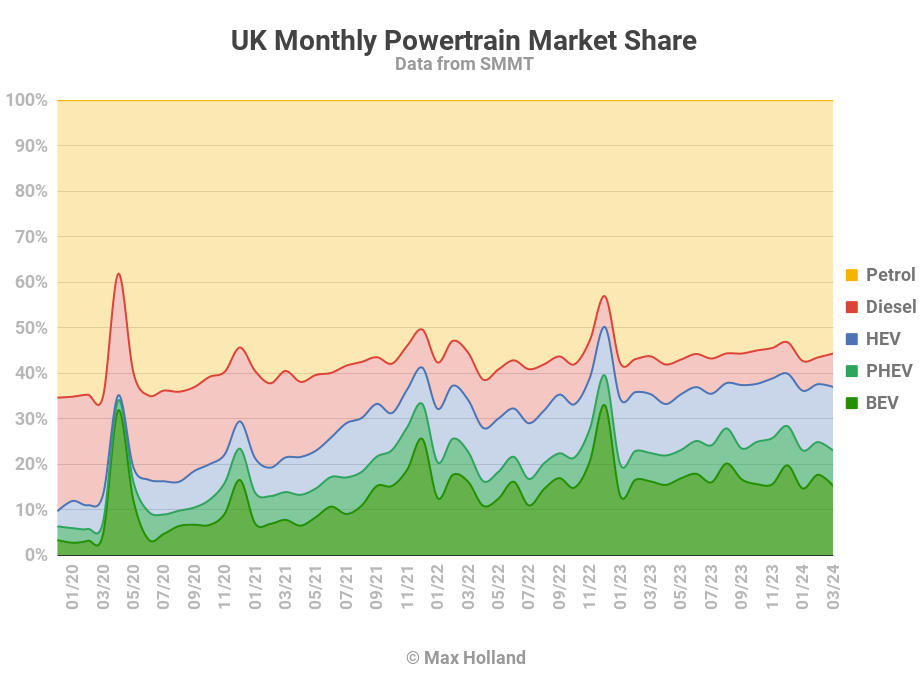

March noticed plugin EVs take 22.9% share of the UK auto market, barely up from 22.4% 12 months on 12 months. Full electrical share fell, whereas plugin hybrid share grew. General auto quantity was 317,786 items, up 10% YoY, although nonetheless far under pre-2020 norms. The UK’s main BEV model was Tesla, forward of BMW.

March’s totals noticed mixed plugin EVs at 22.9% share, with full electrics (BEVs) taking 15.2% and plugin hybrids (PHEVs) taking 7.7%. These examine with YoY shares of 22.4% mixed, 16.2% BEV and 6.2% PHEV.

It is a poor exhibiting for BEVs, dropping 1% share of the market, and up in quantity simply 3.8% YoY, in opposition to broader market progress of 10.4%.

The manufacturers shedding quantity YoY had been Tesla, MG, Volkswagen, and Polestar. This might be as a result of non permanent logistics ebb-and-flow, or it might be demand falling for these manufacturers. Different issues being equal, demand falling might sound unlikely, particularly within the case of MG, which gives the UK’s greatest worth BEVs.

As we mentioned in the Norway report, nonetheless, a cooling of demand may merely be an impact of the UK’s broader financial recession. The “comparatively good worth” BEV manufacturers most definitely to be purchased by atypical of us embody MG on the decrease finish of the pricing spectrum and Tesla in the course of that spectrum. Extraordinary of us, together with those that had been already struggling economically, are likely to get hit the toughest by recessions and maintain off from making massive purchases. The elevated sticker worth of BEVs could make them significantly susceptible in a spending squeeze, greater than lower-priced ICE vehicles.

This may additionally make sense of which manufacturers gained quantity. A number of manufacturers anyway must develop gross sales to satisfy the 22% ZEV mandate, or face massive fines (see final month’s report for dialogue). Of the manufacturers which had been already comfy forward of the mandate, BMW and Mercedes manufacturers stand out as however rising their BEV gross sales YoY at a good clip. This can be as a result of the consumers of those manufacturers are usually much less perturbed by recessionary forces than the median client. It is a speculation — let me know your ideas, and we are going to see if the sample within the months forward seems to assist this, or not. [Editor’s note: These brands and other premium brands are also the auto brands doing better in the US in terms of their own EV market share. The reason is probably in part what Max said, but I also wonder if 1) these automakers feel it is more urgent for them to electrify, and 2) EVs are seen as more competitive by consumers in this segment, and thus considered and bought more. — Zachary Shahan]

A modest counterbalance to the weak spot of BEVs was the relative power of PHEVs, with 37% YoY quantity progress, and claiming an extra 1.5% share of the market, with 7.7% share. HEVs noticed quantity progress of 19%, forward of the market common, although solely half the speed of PHEVs.

Mixed combustion powertrains noticed their share fall to 63.0%, from 64.6% YoY. Their quantity grew 9.3% YoY, underperforming the market common.

{kind=link}

Finest Promoting Manufacturers

Regardless of registering much less quantity than March 2023, Tesla remained the UK’s greatest promoting BEV model for the month.

The Mannequin Y took 80% of Tesla’s quantity, with the Mannequin 3 simply 20%, a ratio of 4:1. Their regular ratio is nearer to 2:1 or 3:1, however Tesla has stated that the Mannequin 3’s provide to Europe from Shanghai has lately been affected by transport delays, because of the troubles within the Purple Sea area.

BMW stays solidly in second place, and Mercedes achieved third, switching locations with MG since final month.

Two notable climbers had been Honda (which we are going to focus on within the subsequent part) and Jaguar, within the 14th and fifteenth spots.

March is normally the UK’s largest month of the 12 months, at round 2 or 2.5× the amount of a traditional month, however Jaguar bought over 5× its typical volumes. This seems to be as a result of they’re each launching the trim-refreshed mannequin of the I-Tempo, and in addition closely discounting the remaining inventory of the outgoing older trim. There is no such thing as a know-how refresh of the re-trimmed I-Tempo, since this can anyway be its final 12 months on sale, and an all-new BEV will launch in 2025.

Let’s now take a look at which manufacturers have been making strikes in Q1 2024 in comparison with This autumn 2023:

The highest 5 manufacturers are solely barely shuffled since This autumn final 12 months, with Mercedes and Audi switching locations. There are extra important modifications additional down the ranks.

The Laggards Doing The Naked Minimal

We’ve famous over latest months that a number of laggard manufacturers had been holding again BEV deliveries in late 2023 (usually the annual peak for BEV market share), to get a head-start on the strict new ZEV mandate for 2024.

Now that the info is in, let’s spotlight essentially the most blatant offenders:

- Toyota went from delivering below 600 items in This autumn 2023 to round 3,500 items in Q1 2024, a change of 6× in quantity. Their BZ4X didn’t get 6× extra enticing over the interval. They jumped from thirty fifth rank (nearly final) in Q3 to tenth in Q1.

- It was the same story for sibling model Lexus, rising quantity from round 100 items to 700 items throughout the interval, climbing from thirty fourth to twenty fifth.

- Honda was equally egregious, going from round 280 items in This autumn to round 1,750 in Q1 (and fifteenth spot).

- Nearly equally skewed had been the Stellantis manufacturers, collectively going from round 2,650 items in This autumn to round 9,200 in Q1. Worst amongst them was Peugeot, going from twentieth place to seventh between the durations.

- Ford was nearly as dangerous, going from round 500 items in This autumn to 1,200 in Q1.

What do I imply by “laggard” manufacturers within the BEV context? I imply manufacturers that are intentionally doing the naked minimal required by the laws to make the transition to BEV.

If you wish to change their stance and get them to cease dragging their ft, my recommendation can be to not assist the present technique of those manufacturers together with your hard-earned cash.

Outlook

Regardless of the rising auto market, the economic system within the UK stays weak. The newest GDP knowledge is from This autumn 2023, at unfavorable 0.2% progress YoY. Headline inflation lowered to three.4%, with rates of interest unchanged at 5.25%. Manufacturing PMI improved to 50.3 factors in March, from 47.5 factors in February. Shopper confidence stays low at unfavorable 21 factors.

The UK auto trade physique, the SMMT (which represents the laggards in addition to others), stated: “Market progress continues, fuelled by fleets investing after two powerful years of constrained provide. A sluggish personal market and shrinking EV market share, nonetheless, present the problem forward. Producers are offering compelling gives, however they will’t single-handedly fund the transition indefinitely. Authorities assist for personal customers — not simply enterprise and fleets — would ship a constructive message and ship a sooner, fairer transition on time and heading in the right direction.”

I agree that the taking part in area between personal customers and fleet consumers ought to be degree, however the UK is the inventor of company capitalism — the concept that huge fleet corporations wouldn’t get extra beneficial tax and profit phrases than personal people is laughable.

The SMMT needs to push the re-introduction of incentives for customers partly as a result of they will cost greater costs to particular person customers than they will to fleets. The latter at all times demand important low cost offers for his or her bulk purchases.

Incentives for customers would additionally enable producers to successfully cost extra for automobiles, which after all is needed by all SMMT members. The laggards would even be helped by incentives boosting relative demand for his or her BEVs, which have to satisfy the ZEV mandate threshold of twenty-two% “zero emission automobiles” (with some wriggle room in observe) in full 12 months 2024.

What are your ideas on the UK’s transition to EVs? Please be a part of within the dialogue under.

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Speak podcast? Contact us right here.

Newest CleanTechnica TV Video

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.