{kind=link}

Join day by day information updates from CleanTechnica on e mail. Or observe us on Google Information!

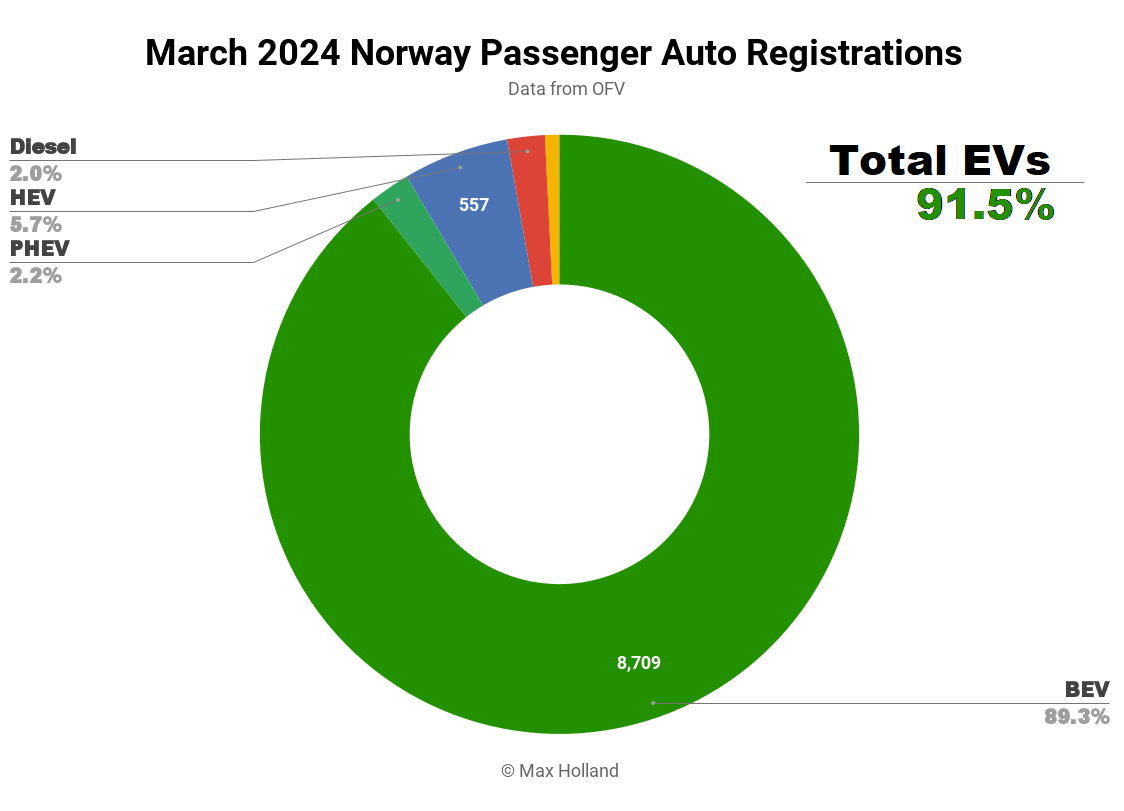

March’s auto market noticed plugin EVs take 91.5% share in Norway, up from 91.1% yr on yr. BEVs alone took virtually 90% share. Total auto quantity was 9,750 models, 50% down YoY, and the bottom March in 15 years. The Tesla Mannequin Y was once more Norway’s finest promoting car.

March noticed mixed EVs take 91.5% share in Norway, comprising 89.3% full electrics (BEVs) and a couple of.2% plugin hybrids (PHEVs). These evaluate with YoY figures of 91.1% mixed, 86.8% BEV and 4.3% PHEV.

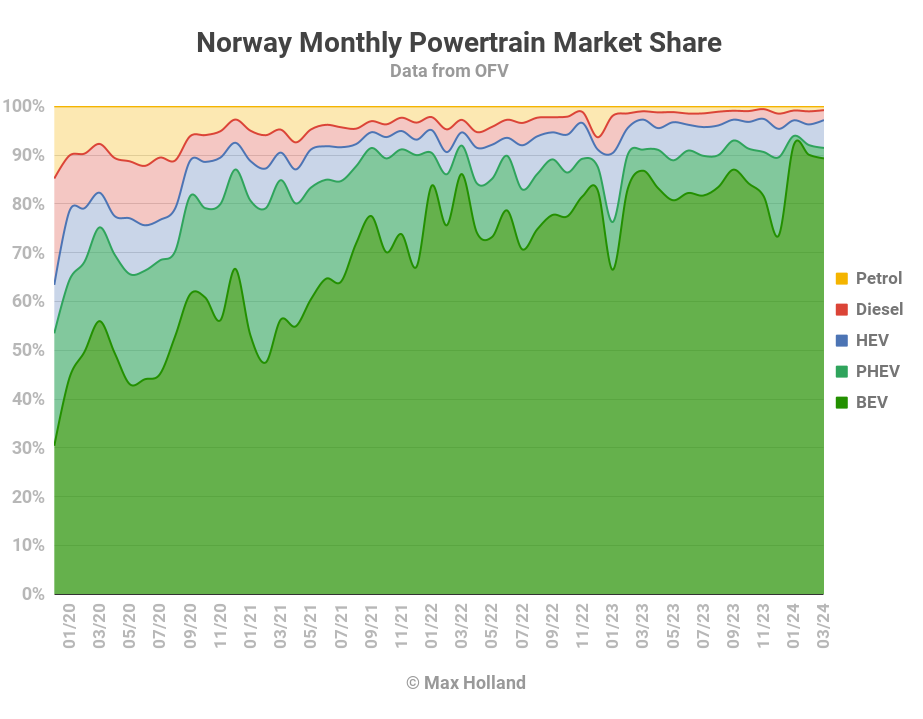

The stability of powertrains continues to be in a hangover from coverage changes that got here into impact on January 1, designed to push consumers from PHEVs to BEVs. PHEV gross sales, averaging 7% share over most of 2023, surged to 16% share in December 2023, forward of the coverage change. Since January, their share has been in hangover, registering 2% share throughout Q1 2024.

BEV share has, in the meantime, elevated to fill the hole, from 83% share over most of 2023 to 90.2% in Q1 2024. PHEV share will get better barely within the months forward, however to not prior ranges, for the reason that coverage is designed to disincentivize them relative to BEVs.

Different powertrain shares are largely unchanged YoY.

By way of volumes, most powertrains roughly halved YoY, proportionate to the halving of the general market. PHEVs had been an outlier, falling to 25% of their YoY quantity.

The general fall in market quantity doubtless displays persevering with weak spot within the broader economic system, with each client confidence and enterprise confidence strongly destructive.

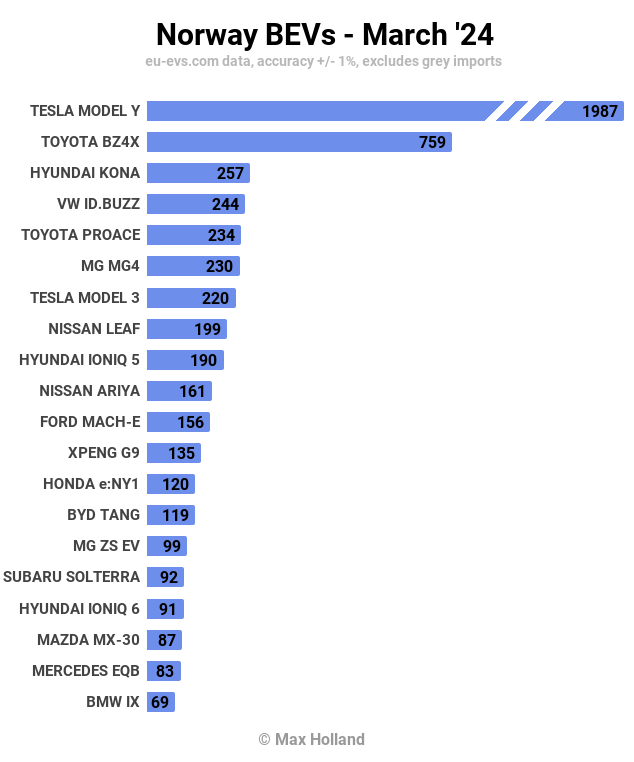

Finest Promoting BEVs

The Tesla Mannequin Y is as soon as once more the very best promoting car in Norway, its eighth consecutive month-to-month pole place. Its March quantity was virtually equal to the subsequent 7 BEVs mixed!

In second place was the Toyota BZ4X, with the Hyundai Kona in third.

A lot of the prime 20 are regulars, with some minor shuffles of rank.

There have been just a few notable climbers, nonetheless. These embrace the Xpeng G9, which gained its highest rank at twelfth from nineteenth final month, and the Honda e:Ny1, which climbed to thirteenth (from 74th).

The remaining climbers had been the BYD Tang, which acquired to 14th (from twenty fourth), and the Mercedes EQB, which ascended to nineteenth (from forty fifth).

So far as I can inform, there have been no new BEV mannequin debuts in March.

The lately debuted BMW iX2 ramped as much as 50 models, from 28 final month. The Peugeot 308 remained flat at 27 models, the identical as February.

Let’s have a look at the three month image:

The Tesla Mannequin Y is thus far forward that its 3 month whole is roughly the equal of the subsequent six BEVs mixed.

The MG4 had a superb climb to sixth, its highest rank but, from ninth within the prior interval (This autumn 2023).

There have been just a few vital tumbles in comparison with This autumn 2023, a lot of them from Volkswagen Group fashions. The Skoda Enyaq fell 18 spots from third to twenty first! Its cousin, the VW ID.4, fell 15 spots from eighth to twenty third. And, sure, their different cousin, the Audi This autumn e-tron, additionally fell, by 11 spots from 14th to twenty fifth.

To not really feel neglected, their junior cousin, the VW ID.3, additionally fell considerably, down 31 spots, from seventeenth to forty eighth!

Has VW Group determined to take a vacation away from Norway this quarter? Soar into the feedback you probably have insights.

I gave an replace on Norway’s fleet transition in final month’s report.

Outlook

I’ve talked about that Norway’s weak economic system is probably going chargeable for the large 50% drop in auto market quantity, together with BEV volumes.

The final GDP replace was from This autumn, and confirmed simply 0.5% YoY progress, from destructive 1.9% in Q3. Inflation diminished barely to 4.5% in February (newest), from 4.7% in January. Rates of interest remained flat at 4.5% (February, newest). Manufacturing PMI worsened to 50.8 factors in March, from 51.9 factors in February. As I said earlier, each client confidence and enterprise confidence stay traditionally weak.

Norway’s OFV agrees that the financial circumstances are accountable for the large drop in auto volumes, stating: “New automotive gross sales, which are sometimes a form of temperature gauge on folks’s funds, replicate the monetary challenges many are experiencing…” (OFV assertion, machine translation).

The OFV additionally says that:

“[N]ow most individuals select smaller and extra reasonably priced new automobiles than previously 5 or 6 years… this may have an effect on new automotive gross sales going ahead… Lots of the main automotive producers now see a big market in smaller, inexpensive automobiles, not least electrical automobiles, and are turning elements of their manufacturing in direction of this. … Sooner or later, there shall be many new smaller and extra inexpensive electrical automobiles on the Norwegian market. On the identical time, there shall be automobiles that fulfill many individuals’s wants, and that may rapidly problem manufacturers and fashions which have lengthy been effectively established in Norway.” (Machine translation)

That is a gorgeous concept, and common readers will know that I’ve been banging this drum for a very long time, however I see no indicators of it truly taking place but. At the least to not the extent it might and ought to be taking place given the fast fall in costs of BEV batteries and powertrains. An October report from JATO says that 2022 noticed the precise reverse pattern:

“[European prices] proceed to rise…. To purchase an EV, shoppers would wish to spend no less than €18,285 in Europe and €24,400/$26,500 within the US. That is 92% and 146% dearer than what they might pay for the most affordable combustion automotive accessible, respectively … largely because of the trade’s continued concentrate on premium EVs forward of extra extensively inexpensive mid-range [vehicles] … many Western carmakers elevated their costs whereas shoppers had been made to attend longer for brand new autos. For a lot of OEMs this technique paid off. In 2022, most of those firms reported fewer models bought, however increased income and file earnings.” (JATO’s “EV Worth Hole” report, October 2023)

As to the OFV’s closing sentiment that this attainable emergence of extra inexpensive BEVs might “rapidly problem manufacturers and fashions which have lengthy been effectively established in Norway [and Europe]” (and which — I’ll add — have for many years dragged their toes on the EV transition), effectively, we will solely hope that karma will certainly meet up with them.

What are your ideas on Norway’s EV transition? Please be part of within the dialog under.

Have a tip for CleanTechnica? Need to promote? Need to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Newest CleanTechnica TV Video

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.