{kind=link}

The specialised deepwater oil & gasoline and floating offshore wind segments will share most of the similar stakeholders and provide chains, competing for more and more scarce sources.

To obtain a full model of Inteletus evaluation, click on right here

The established floating manufacturing section is forecast to expertise continued progress by means of this decade, driving demand for, amongst different issues, moorings, subsea programs, umbilicals, risers, flowlines and the big anchor handlers and subsea help vessels that can set up and keep the weather.

On the similar time, the floating wind section will transfer from demonstration and pilot scale initiatives to pre-commercial and business scale arrays and can eat massive quantities of mooring elements and dynamic electrical cables in addition to the big anchor handler and subsea help vessel capability that can set up and keep the weather.

A lot of the brand new floating wind provide chain will leverage the present floating oil & gasoline provide chains. Gamers skilled in deepwater oil & gasoline operations, whether or not builders, EPCI contractors or element and repair suppliers, will discover a rising alternative to leverage their expertise within the rising floating wind section.

These are the findings of a brand new whitepaper produced by Intelatus World companions entitled “Floating Manufacturing and Floating Wind – more and more shut segments”.

A Rising Floating Manufacturing Phase

Based on the most recent Intelatus deepwater floating manufacturing forecast, floating manufacturing exercise within the oil & gasoline sector is about to develop at a median 25 floaters per 12 months by means of 2030, and the foundations are in place for continued exercise by means of the subsequent decade.

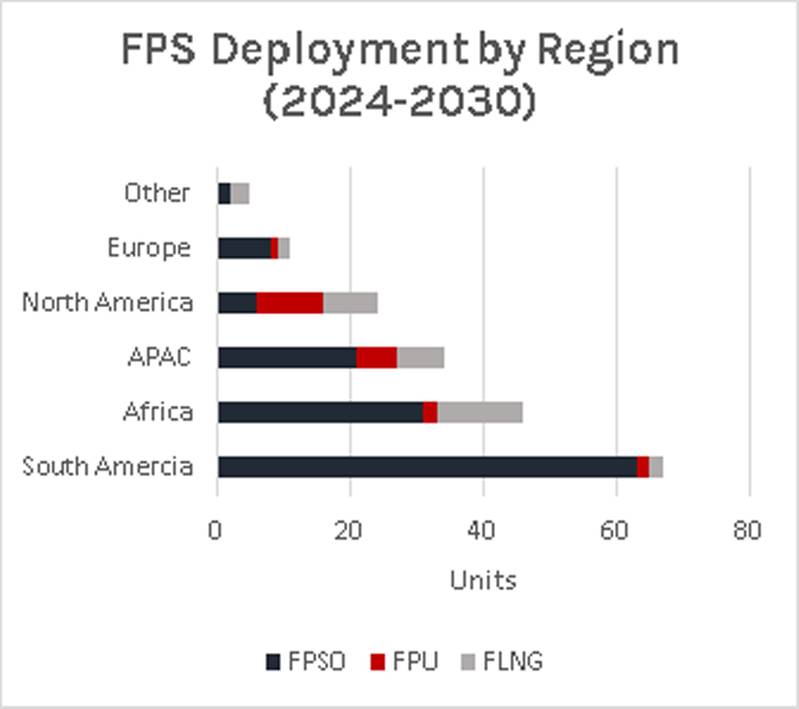

There will likely be over 260 floating manufacturing programs put in globally by the tip of 2023. Over 185 new floaters will likely be put in by the tip of 2030, of which 70% will likely be FPSOs, shut to twenty% FLNGs and floating manufacturing models with out storage (semi-subs, TLPs and spars) over 10%.

Supply: Intelatus

Supply: Intelatus

We forecast that greater than two thirds of recent floating manufacturing models put in between 2024 and 2030 will likely be situated in South and Central American nations, of which Brazil and Guyana will account for round 90% of the share of models. FPSO know-how dominates the area’s FPS demand.

In all, 18 nations in West and East Africa are anticipated to obtain new FPSOs, FLNGs and FPUs between 2024 and 2030. Africa is forecast to be dwelling to the biggest variety of FLNGs in our forecast, accounting for over 35% of worldwide installations.

The third most energetic floating manufacturing area from 2024-2030 is forecast to be Asia Pacific. Over 60% of the exercise within the area is anticipated to return from FPSOs, with FLNGs and FPUs every accounting for round 20% of the models.

Over 80% of the exercise forecast for North America will likely be situated within the U.S and Mexican Gulf of Mexico. The area will likely be dwelling to the biggest variety of FPUs, accounting for near half of our international forecast.

A Phase in Transition

We’re noting a transition within the enterprise fashions of many floating manufacturing system house owners. Modifications embrace deploying the most recent applied sciences to decarbonize floating manufacturing operations and transition floating manufacturing exercise right into a wider floating vitality enterprise that leverages the abilities and classes learnt from deepwater oil & gasoline initiatives into the rising floating wind section, with measures together with:

- The use gasoline and discount in routine flaring, whether or not by means of liquefaction or pipeline export.

- The elevated deployment of carbon seize applied sciences coupled with the reinjection of carbon dioxide into wells (e.g. Petrobras plans to inject CO2 into pre-salt storage).

- The broader scale adoption of mixed cycle energy era and topside electrification by a number of main FPSO house owners. Sources of energy investigated by some builders for floating manufacturing programs embrace renewable vitality, corresponding to offshore wind.

- Leveraging Trade 4.0 applied sciences to enhance manufacturing unit operations and upkeep efficiency, together with IoT connectivity, digital twins and autonomous operations.

- An rising floating manufacturing section – the manufacturing and storage of low and 0 emission vitality carriers, corresponding to methanol and ammonia. One thrilling growth leverages Era IV small modular nuclear reactors to supply the ability and warmth required to desalinate seawater, energy electrolyzers and different manufacturing, storage and offloading programs. Ideas are being developed in South Korea and Europe.

- Lastly, we’re seeing a development of sure key gamers within the floating manufacturing section to leverage their experience for executing difficult and enormous initiatives in deep water into the floating wind area, together with Petrobras, Shell, TotalEnergies, Equinor, CNOOC, SBM Offshore, MODEC and BW Offshore.

Competing for the Identical Provide Chains

The expansion in exercise in each the floating manufacturing and the floating wind segments will drive elevated demand for engineering companies, shipyard and port capability, mooring system provide, dynamic subsea cables and specialist set up vessels. We’re forecasting some potential provide chain bottlenecks on account of the elevated exercise.

To point out how floating manufacturing and floating wind initiatives will compete for related sources, we are going to use a high-level easy instance evaluating a “typical” FPSO with a “typical” floating wind undertaking deploying typical moorings.

As the standard oil and gasoline floating manufacturing section grows, the floating wind section will transfer from demonstration and pilot scale initiatives to pre-commercial and business scale arrays and can eat massive quantities of mooring elements and dynamic electrical cables in addition to the big anchor handler and subsea help vessel capability that can set up and keep the weather.

As the standard oil and gasoline floating manufacturing section grows, the floating wind section will transfer from demonstration and pilot scale initiatives to pre-commercial and business scale arrays and can eat massive quantities of mooring elements and dynamic electrical cables in addition to the big anchor handler and subsea help vessel capability that can set up and keep the weather.

Picture courtesy Gazelle Wind EnergyIf we apply this straightforward “rule of thumb” strategy to our floating manufacturing and floating wind mooring pre-lay forecast by means of 2030, floating wind accounts for round 30% of the entire mooring line amount required and practically 50% of the anchor quantity. This will likely be a problem for the present greater spec vessel provide aspect to accommodate, given its present excessive utilization. The Intelatus Floating Wind Set up Vessel Forecast analyses the business and technical potential vessel capability and functionality gaps intimately in addition to why the business situations don’t but actually exist for sustained new constructing exercise.

Floating wind is a brand new know-how the place engineers proceed to seek for progressive methods to ship business scale initiatives. Nonetheless, no less than within the short- to mid-term, builders might want to depend on present applied sciences and provide chain capabilities to ship business scale wind farms, applied sciences which have been developed over years within the deepwater floating manufacturing section.

Gamers skilled in deepwater oil & gasoline operations, whether or not builders, EPCI contractors or element and repair suppliers, will discover a rising alternative to leverage their expertise within the rising floating wind section.

Nonetheless, the stakeholders in each segments ought to pay attention to a forecast scarcity and subsequently elevated competitors for provide chain sources.

To obtain a full model of Inteletus evaluation, click on right here