{kind=link}

Written by

Marine Log Workers

Picture: BOEM

Enterprise consultancy Intelatus International Companions has been looking on the a lot mentioned “readjustment” within the U.S. offshore wind sector and placing issues into perspective.

The beginning of 2024 marks a interval the place the “readjustment” of the U.S. wind phase appeared to turn into extra obvious, says the agency. At a federal degree, practically 9 gigawatts (GW) of lease potential within the Central Atlantic and Oregon handed additional hurdles to be auctioned within the subsequent 12 or so months. Together with these two areas, BOEM is dedicated to leasing additional websites within the Gulf of Mexico, and the Gulf of Maine in 2024/2025. When added to the potential capability of these leases beforehand awarded, the overall potential leased will quantity to round 80 GW, of which near 26 GW is at some point of the federal allowing course of.

At a state degree, notes Intelatus, New Jersey chosen 3.7 GW of capability from the Attentive Power Two and Main Mild Wind tasks. In an indication of the instances, Connecticut, Massachusetts and Rhode Island pushed again the submission date for his or her 6.8 GW of solicitations to March, to permit builders to hunt additional steering from the Inner Income Service concerning IRA associated tax credit, which embody the ten% Power Communities bonus.

Tax credit score monetization is a peculiarity of the U.S. wind phase and is vital to the economics of many tasks. This difficulty was touched on in a current investor presentation by the CEO of Ørsted, the developer sitting on the most important offshore wind portfolio within the U.S. Regardless of remaining centered on Northeast and Mid-Atlantic mission growth, important capability is presently underneath evaluate attributable to provide chain capability, competency and value inflation, excessive rates of interest and lack of readability on tax credit score monetization. South Fork (2024) and Revolution Wind (2025) are anticipated to hitch Block Island to offer the corporate three operational U.S. wind farms. The event of Dawn Wind stays contingent on a profitable offtake settlement from the New York 4 solicitation attributable to be introduced shortly and which incorporates improved monetary phrases permitting builders to mitigate a number of the particular dangers related to U.S. tasks. The 4 GW Bay state lease space additionally stays in growth. Within the Mid-Atlantic, Ørsted stays centered on divestment or an “different alternative for worth creation” for Ocean Wind 1 and a couple of, has withdrawn from its agreements to promote energy to Maryland from Skipkack 1 and a couple of (though it continues to mature the mission) and continues to advance its Backyard State lease with minimal spend.

Ørsted is just not alone in questioning the financials of U.S. offshore wind sector tasks. After reorganizing its Empire Wind and Beacon Wind portfolio, whereby Equinor takes full management of Empire Wind and BP assumes full possession of Beacon Wind, Equinor has put Empire Wind 2 on maintain, cancelling a number of provide chain commitments. Nonetheless, the corporate nonetheless goals to safe an offtake within the New York 4 solicitation for Empire Wind 1 and to advance the mission.

Whereas there have been excessive profile “dangerous information” headlines, a number of massive tasks are maturing, and Intelatus expects to see important offshore building happening in 2024 and 2025. In a sign of the challenges going through growing home floating wind provide chains, California issued a draft report addressing the numerous manufacturing, port, building and logistics vessel and transmission challenges to be addressed within the coming years. Greater than $10 billion of port and manufacturing infrastructure funding is estimated to be required amongst different enabling investments.

INTELATUS FORECASTS 110 GW BY 2050

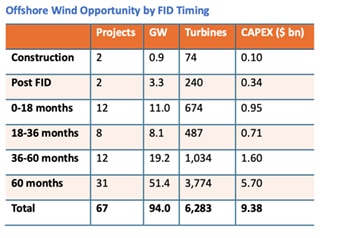

Intelatus says that it maintains its forecast of over 65 tasks that can set up round 94 GW of capability on this and the subsequent decade and a complete 110 GW by 2050.

The 90 GW forecast capability would require capital expenditure amounting to round $290 billion to deliver onstream, a recurring annual operations and upkeep spend of $9.4 billion as soon as delivered, and over $40 billion of decommissioning expenditure on the finish of business operations.