{kind=link}

The worldwide safety hole has been trending upwards since 2010. By 2025, Asia and the Pacific is predicted to account for practically half of the entire, reaching US$0.93 trillion, the identical quantity because the safety hole for the world in 2010. Picture: PwC Bermuda

Historically, funds from donor nations and worldwide organisations performed a major function in post-disaster reduction capital. Nevertheless, political and administrative elements typically delay capital switch and hinder response efforts.

Parametric insurance coverage provides a faster various. Payouts are computerized, enabling well timed rehabilitation and minimising long-term socio-economic impacts, stated Ricciardi.

In areas of Asia the place growth funds are restricted and overseas support unreliable, parametric insurance coverage may fill a important hole by decreasing uninsured dangers.

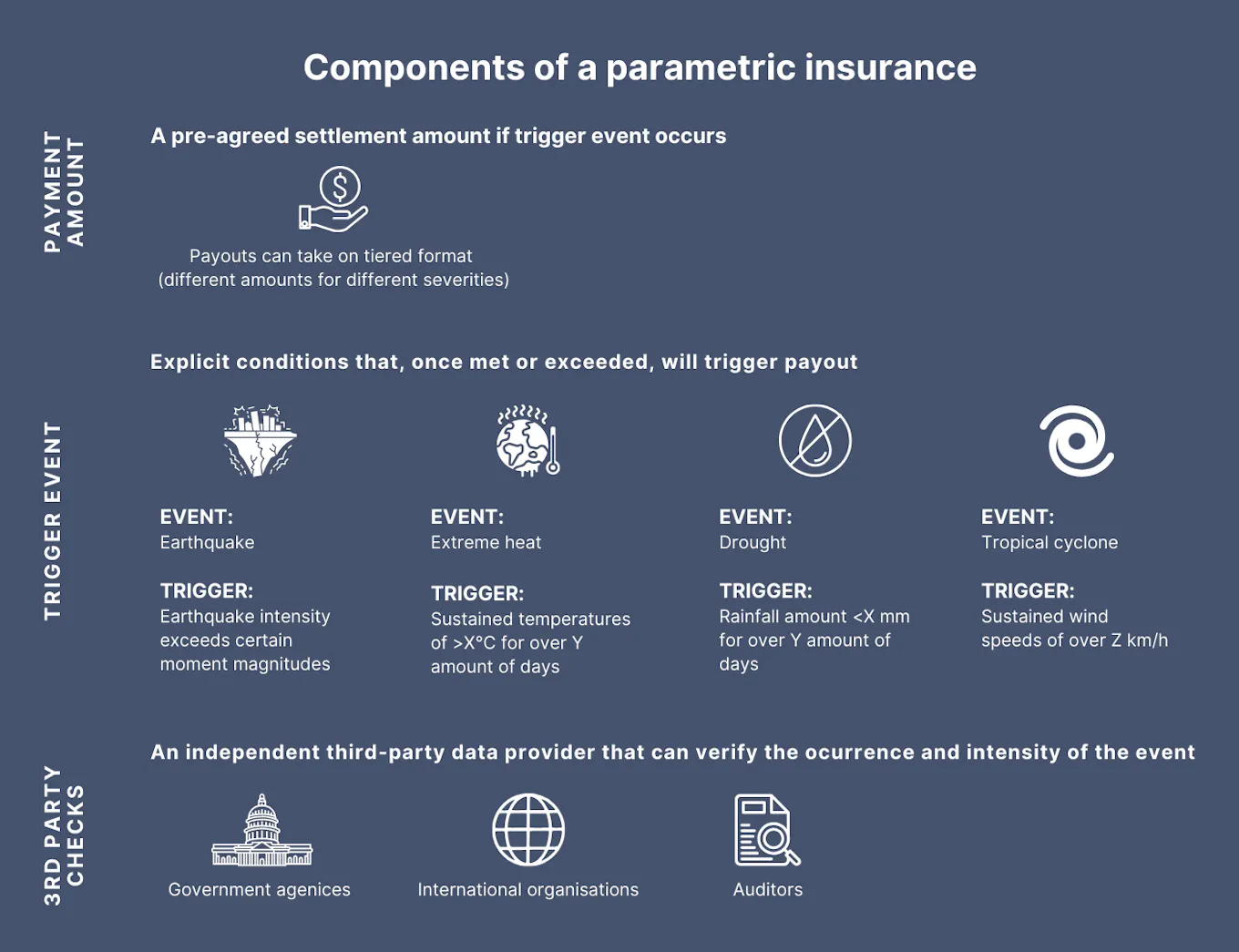

What’s parametric insurance coverage?

Parametric insurance coverage depends on a set of predefined parameters, or occasion triggers. When these parameters are met or exceeded, the insurance coverage cowl is triggered, and a payout is made routinely, no matter precise bodily losses sustained.

A parametric insurance coverage coverage has three key parts: a pre-agreed cost quantity, a predefined set off occasion, and third-party checks to confirm occasion incidence.

Picture: Eco-Enterprise

How does parametric insurance coverage differ from conventional insurance coverage?

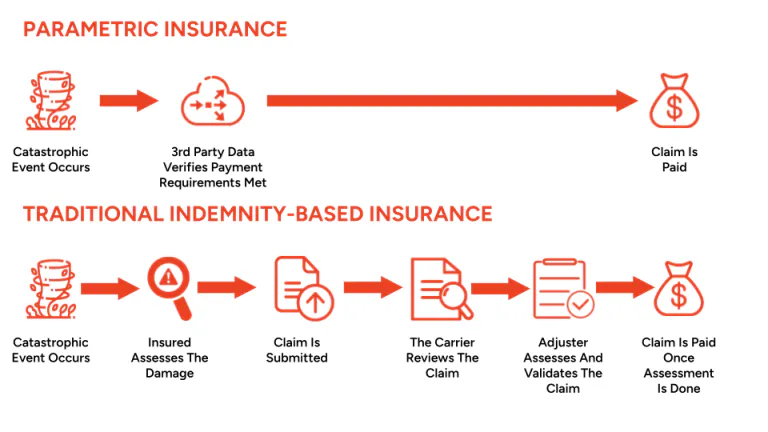

Conventional insurance coverage is indemnity-based, which suggests claims are paid solely after damages have been assessed and verified, and settlement can take months to years.

Comparatively, little administration and minimal proof of precise losses are required for parametric insurance coverage. An impartial third get together solely must confirm that the phrases for cost have been met. The streamlined claims course of permits a lot sooner payouts, with the funds being disbursed inside a month.

Parametric insurance coverage provides a extra streamlined course of as in comparison with conventional indemnity-based insurance coverage. This enables payouts to succeed in affected communities a lot sooner, which aids essential restoration efforts. Picture: Danger and Insurance coverage Schooling Alliance

Parametric insurance coverage is usually designed to enrich, quite than change, conventional insurance coverage merchandise. It goals to cut back danger publicity by masking areas not insured by standard merchandise.

“Policyholders can search the perfect of each worlds with a hybrid construction that mixes parametric and traditional insurance coverage. This enables for a quick cost following the insured occasion for instant restoration, while the complete quantity of injury might be assessed subsequently,” stated Christopher Au, director for international brokerage WTW’s Asia-Pacific Local weather Danger Centre.

Why is parametric insurance coverage more and more engaging in Asia?

The elimination of the claims verification and adjustment course of permits funds to succeed in policyholders a lot sooner. This considerably reduces the monetary burden of post-event response, which is essential for disaster-prone Asia.

As an illustration, when tremendous Storm Rai – recognized domestically as Storm Odette – struck the Philippines in 2021, an influence utility firm in Cebu was paid inside simply 12 days after the occasion by international insurance coverage agency Swiss Re, below a parametric insurance coverage product.

In line with the coverage’s phrases, reported to be a “cat-in-a-box” kind construction, the payout was triggered when the storm’s sustained wind speeds exceeded predefined ranges whereas passing by way of the area. These funds may then be used for restoration efforts, minimising disruptions to a vital service.

“Cat-in-a-box”

“Cat-in-a-box” is the most well-liked type of parametric insurance coverage construction, resulting from its simplicity of comprehension and execution.

“Cat” refers back to the disaster the policyholder is being insured towards, resembling typhoons or earthquakes. The field demarcates a selected, predefined space which the insurance coverage will cowl, though it could take any form.

If the disaster meets each the pre-agreed parameter threshold and happens inside the field, a payout will likely be triggered.

Speedy liquidity for post-disaster response is more and more pertinent for Asia, which has borne the brunt of local weather catastrophes. The area is now 25 instances extra probably to be affected by pure disasters than Europe, in response to the ADB.

“The continued improve in losses from pure catastrophes and the rise in costs for standard insurance coverage has resulted in a tightening of common phrases and situations, and corporations throughout Asia must assume extra fastidiously about their present danger switch preparations,” stated Au.

Parametric insurance coverage additionally provides protection for dangers not insured by conventional market merchandise.

As an illustration, Sri Lanka’s coastal shrimp farms have been insured towards 4 climate dangers – earthquakes, typhoons, extreme rainfall, and warmth stress – below Asia’s first four-peril parametric insurance coverage product launched by WTW.

These climate occasions aren’t coated by present insurance coverage merchandise, though climate dangers pose the most typical threats to shrimp farming.

The product was designed for Taprobane Seafood Group, the nation’s main seafood firm. It’s anticipated to assist Taprobane’s growth of sustainable shrimp farming, which can present native employment alternatives, whereas supporting aquaculture progress and easing meals safety issues.

Downsides to parametric insurance coverage?

Whereas divorcing precise losses from claims settlements expedites payouts, this mechanism additionally leads to foundation danger – the distinction between the precise monetary impacts suffered by the insured get together, and the payout obtained below the insurance coverage coverage.

Restoration efforts may even be undermined if the payout is inadequate to cowl losses. Within the worst circumstances, insured events may endure losses with out parameters even being triggered.

This was the case for Malawi’s 2016 drought, the place no payouts had been triggered regardless of some 6.5 million folks assessed as needing help. The insurer had used a defective mannequin which severely underestimated the variety of people affected by the drought.

Following a reassessment, US$8 million was lastly paid out to Malawi’s authorities in January 2017, greater than half a yr after requests had been filed. Nevertheless, the quantity was deemed to be “too little, too late”, as the federal government was compelled to make use of different means to cowl financial losses estimated at US$395 million.

Since parametric insurance coverage is a comparatively new growth, the shortage of regulatory and governance frameworks has additionally hindered adoption.

In jurisdictions with out separate insurance policies for parametric insurance coverage, insurance policies are topic to the identical indemnity legal guidelines as conventional insurance coverage, slowing down cost.

Nevertheless, key developments resembling regulatory sandboxes and centralised platforms for product provides are anticipated to streamline the method in Asia.

“There may be all the time inertia and concern when making an attempt one thing new. Consolation and observe file with the reliability of the product and method is vital, and that is enhancing over time,” stated Au.

The parametric insurance coverage panorama in Asia

Presently, China dominates the area’s parametric insurance coverage market and is predicted to stay so till 2028, reaching a market worth of US$1.6 billion.

A number of initiatives, such because the Southeast Asia Catastrophe Danger Insurance coverage Facility (SEADRIF), have additionally been developed to safeguard the area towards climate-driven hazards. SEADRIF is the primary regional disaster danger insurance coverage. As an illustration, it supplied protection towards flood dangers in Laos in August 2023, with two payouts totalling US$1.5 million for flood reduction efforts.

There are additionally smaller scale microinsurance initiatives for particular person stakeholders. Usually, these goal smallhold farrmers who might not possess intensive funds, however nonetheless have belongings to insure.

In India, a microinsurance undertaking for local weather change and catastrophe resilience has been carried out to increase local weather change danger protection to low-income households in rural areas. Supported by the ADB, the fund has disbursed US$59.5 million as of March this yr.

Individually, investments have been made into infrastructure resembling satellites to seize information on the causes and impacts of pure catastrophes. In Southeast Asia, these developments have helped construct up a data profile of the area, enabling extra correct insurance coverage formulation to cut back foundation danger.

“Enhancements in information analytics, distant sensing know-how, and local weather modelling will improve the precision of parametric triggers, making insurance coverage merchandise extra customised and efficient,” stated Ricciardi.

A sustainable answer to protect towards local weather dangers?

Parametric insurance coverage won’t be the panacea for cover towards climate-related disasters. Consultants have warned that with local weather change inflicting extra harm than projected, and too little cash being spent on defending populations, such insurance coverage initiatives may battle in the long term.

For instance, Kenya’s Livestock Insurance coverage Programme paid out 1.2 billion Kenyan shillings (US$8.8 million) for drought damages between 2015 and 2021, however solely collected 1.1 billion Kenyan shillings (US$8.1 million) in premiums. The scheme has since been changed.

“Parametric insurance coverage provides a short lived answer by offering instant funds post-disaster, making certain that communities can bounce again rapidly whereas longer-term adaptation measures are carried out,” stated Ricciardi.

A wider view on danger additionally helps the corporate to evaluate the entire price of danger, so that elevated investments in adaptation and resilience can be understood as decreasing the necessity for danger switch, added WTW’s Au.